The 2008 financial crisis almost destroyed the global economy. Andrew Ross Sorkin's fly-on-the-wall account reveals the human psychology behind market collapses.

Hyle Editorial·

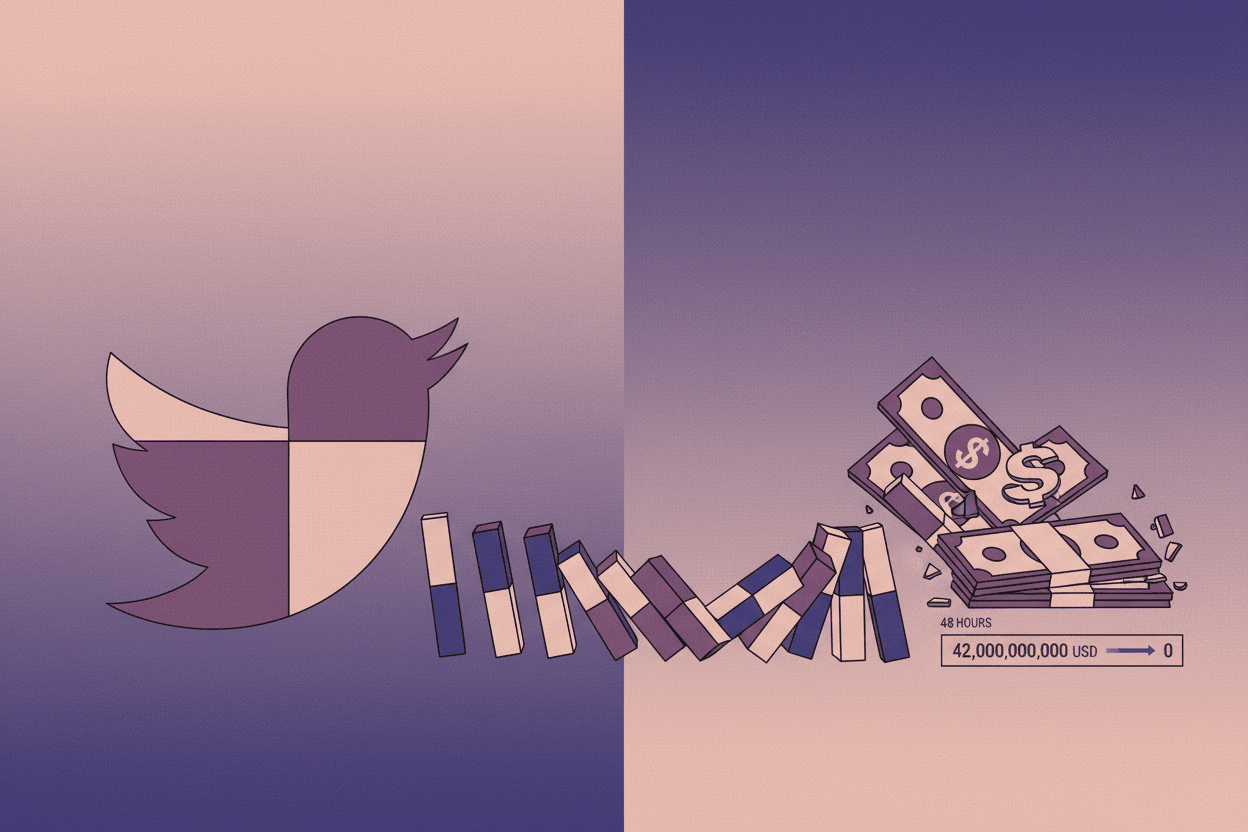

On September 15, 2008, Lehman Brothers filed for bankruptcy—the largest corporate failure in American history. Within 72 hours, the global financial system came within hours of total collapse. AIG required an $85 billion emergency bailout. Money market funds "broke the buck." The commercial paper market froze solid. Yet in his masterwork Too Big to Fail, Andrew Ross Sorkin reveals something more disturbing than the numbers: the same psychological patterns that triggered the Great Depression of 1929 nearly destroyed modern capitalism.

The terrifying truth? We've seen this movie before. Mark Twain's famous quip—"history doesn't repeat itself, but it often rhymes"—captures something essential about financial crises that Sorkin's reporting makes viscerally clear. The bankers, regulators, and politicians who stood at the epicenter of 2008 weren't fundamentally different from their 1929 counterparts. They made the same cognitive errors. They clung to the same dangerous illusions. And the rhyming patterns Sorkin documents suggest we may be composing the next verse right now.

Sorkin's fly-on-the-wall narrative begins months before the collapse, inside the walnut-paneled conference rooms where Wall Street's titans gathered to confront a crisis they still refused to believe was possible. What emerges is a portrait of collective denial so profound it almost feels engineered.

In March 2008, Bear Stearns CEO Alan Schwartz went on CNBC to assure investors his bank was "well capitalized." Two days later, Bear Stearns collapsed into the arms of JPMorgan for $2 per share—a 98% discount from its 52-week high. The pattern repeated with Lehman's Dick Fuld, who rejected rescue offers until his only option was bankruptcy.

[!INSIGHT] The critical failure wasn't lack of information—it was the inability to process information that contradicted deeply held beliefs about market rationality. Sorkin shows how even the most sophisticated financial minds succumbed to normalcy bias.

Sorkin captures a haunting moment from April 2008, when Treasury Secretary Hank Paulson convened a dinner at the St. Regis Hotel. The assembled CEOs of America's largest banks were asked to consider worst-case scenarios. Most dismissed the exercise as unnecessarily pessimistic. Six months later, nine of the ten banks represented would require federal rescue.

“"We can't solve problems by using the same kind of thinking we used when we created them.”

— Albert Einstein

The parallels to 1929 are unmistakable. In the weeks before the October crash, Yale economist Irving Fisher famously declared that stock prices had reached "what looks like a permanently high plateau." The smartest minds of each era made identical errors of extrapolation, assuming that recent stability proved permanent stability.

Leverage: The Invisible Catalyst

If denial provided the psychological precondition for crisis, leverage provided the explosive material. Sorkin's reporting reveals the staggering extent to which Wall Street had amplified risk through complex instruments that even their creators struggled to understand.

In 1929, investors could buy stocks on 90% margin—putting down $10 to control $100 worth of shares. When prices fell, margin calls forced cascading liquidations. In 2008, the leverage was more sophisticated but equally dangerous. Lehman Brothers operated with leverage ratios exceeding 30:1. A mere 3% decline in asset values would wipe out shareholder equity entirely.

The innovation of mortgage-backed securities and credit default swaps had distributed risk throughout the global financial system—a feature that was supposed to make crises impossible. Instead, it made them contagious. When housing prices began falling in 2006-2007, the losses multiplied through leveraged balance sheets everywhere.

[!NOTE] Sorkin documents how AIG Financial Products, a small division of the insurance giant, had sold hundreds of billions in credit default swaps without setting aside adequate reserves. The division's London office had just 377 employees but nearly brought down a company with 116,000 workers and $1 trillion in assets.

The 1929 parallel is again striking. Investment trusts—the era's version of pooled investment vehicles—had proliferated in the late 1920s, creating complex ownership structures that amplified losses when the market turned. In both eras, financial innovation outpaced financial understanding.

The Social Contagion of Panic

Perhaps Sorkin's most valuable contribution is his granular documentation of how panic spreads through elite networks. His minute-by-minute account of the weekend of September 13-14, 2008—when Wall Street's CEOs gathered at the New York Fed to decide Lehman's fate—reads like a psychological thriller.

What becomes clear is that panic operates through social channels. When Morgan Stanley's John Mack received a call from a hedge fund friend reporting that counterparties were pulling business, he knew his firm was next. When GE's Jeff Immelt called to warn that his company couldn't access commercial paper markets, Paulson understood the crisis had jumped from Wall Street to Main Street.

“"In a crisis, the only thing more expensive than information is the lack of it.”

— Andrew Ross Sorkin

The 1929 crash followed similar patterns of social contagion. Crowds gathered outside the New York Stock Exchange. Rumors spread through brokerage houses. Telephone operators were overwhelmed with sell orders. The mechanisms of communication had changed, but the human dynamics remained identical.

[!INSIGHT] Financial panics are fundamentally social phenomena. They spread through relationships, phone calls, and whispered warnings—not through rational analysis of market fundamentals. Understanding this social dimension is essential for recognizing when the next panic is building.

The Rhyme Detector: Reading the Patterns

Sorkin's work offers an implicit methodology for recognizing crisis patterns before they fully materialize. The signals he documents—excessive leverage, widespread denial, regulatory fragmentation, and concentration of risk in novel instruments—are diagnostic tools that attentive readers can apply.

Consider the current landscape. As of 2024, global debt levels exceed $300 trillion—significantly higher as a percentage of GDP than in 2008. New financial instruments have proliferated, from private credit to cryptocurrency derivatives. The smartest people in finance assure us these innovations have made the system more resilient.

Sorkin's history suggests we should be skeptical. The patterns he identifies—denial among elites, leverage accumulating in shadowy corners, and the social dynamics of panic—are rhyming if not repeating. The specific instruments may differ, but the underlying human behaviors remain consistent across centuries.

“[!NOTE] After the 2008 crisis, Congress passed the Dodd-Frank Act to prevent future bailouts. Yet the concept of "too big to fail" has arguably grown larger. The top four U.S. banks now control assets exceeding $9 trillion”

— roughly 40% of all U.S. banking assets—compared to $3.6 trillion and 35% before the crisis.

The Enduring Relevance

Too Big to Fail has become essential reading not because it explains what happened—that much has been documented elsewhere—but because it shows how it happened at the human level. Sorkin's fly-on-the-wall access reveals the psychological states, social pressures, and cognitive limitations that drive decision-making under extreme stress.

For investors, policymakers, and citizens, the value lies in pattern recognition. The next crisis won't look exactly like 2008 or 1929. The triggers will be different—perhaps commercial real estate, perhaps sovereign debt, perhaps something not yet visible. But the patterns of denial, leverage, and contagion will rhyme.

Key Takeaway

Financial crises follow predictable human patterns, not predictable timelines. By understanding the psychology of denial, the mathematics of leverage, and the sociology of panic that Sorkin documents, readers gain the pattern-recognition tools necessary to recognize the next crisis while there's still time to prepare.

Sources: Andrew Ross Sorkin, "Too Big to Fail: The Inside Story of How Wall Street and Washington Fought to Save the Financial System—and Themselves" (2009); Federal Reserve Historical Data; Financial Crisis Inquiry Commission Report (2011)

This is a Premium Article

Hylē Media members get unlimited access to all premium content. Sign up free — no credit card required.