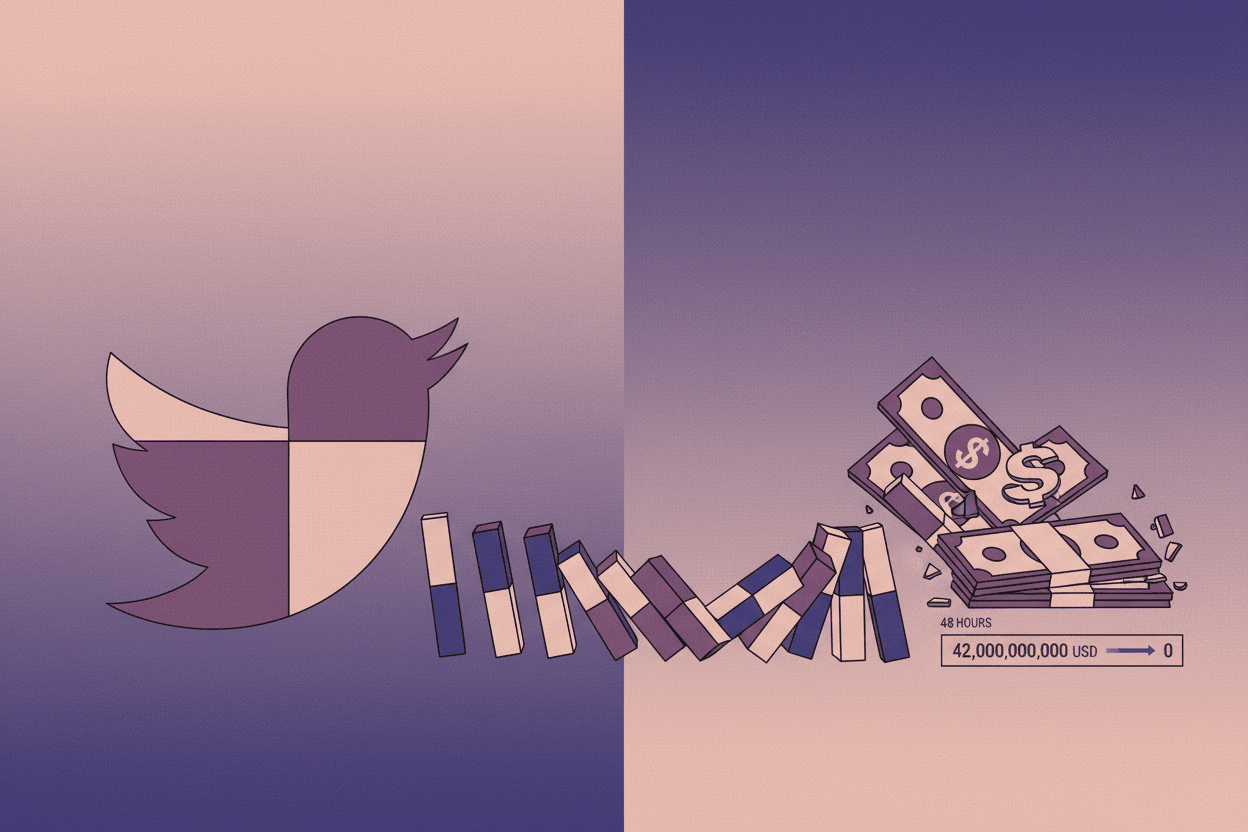

Silicon Valley Bank lost $42 billion in 48 hours—not from bad loans, but from a Twitter-fueled panic. Discover why your bank is always one viral post away from collapse.

Hyle Editorial·

Silicon Valley Bank did not collapse because of bad loans. It collapsed because 42,000 people saw a tweet, opened their banking apps, and moved $42 billion in 48 hours. The bank run of 2023 was the first in history driven by group chat. The mechanism is identical to 1929. Only the speed changed.

In 1933, it took weeks of newspaper headlines and physical lines around city blocks to drain the American banking system. In March 2023, it took a single Wednesday afternoon for venture capitalists to coordinate the largest bank run in U.S. history through Twitter threads and Slack channels. By the time regulators closed SVB on Friday, depositors had withdrawn 94% of the bank's deposits in under 60 hours.

The terrifying reality? Every bank with more depositors than cash on hand—which is all of them—is vulnerable to the same mechanism. Your savings account is not a vault. It is a bet that not everyone will ask for their money back at the same time.

The Anatomy of a Bank Run: How Fractional Reserve Banking Creates Fragility

To understand why bank runs happen, you must first accept an uncomfortable truth: banks do not keep your money. They lend it.

When you deposit $1,000 at First National Bank, the bank might keep $100 in reserves and lend $900 to a homebuyer, a business owner, or a credit card holder. This is fractional reserve banking—the foundation of modern credit economies. It works beautifully when depositors trust the system. It catastrophically fails when that trust cracks.

The Liquidity Mismatch Problem

Banks have short-term liabilities (your deposit, which you can withdraw anytime) and long-term assets (a 30-year mortgage that cannot be called in). This structural mismatch means no bank can survive a coordinated withdrawal. If every depositor at JPMorgan Chase demanded cash tomorrow, the largest bank in America would collapse by Thursday afternoon—despite having trillions in assets.

[!INSIGHT] A bank's solvency (assets exceed liabilities) and its liquidity (cash on hand) are completely different things. SVB was solvent on paper when its run began. It died because it couldn't liquidate assets fast enough to meet withdrawal demands.

The 2023 SVB crisis exposed this dynamic with brutal clarity. When interest rates rose, the bank's portfolio of long-term Treasury bonds lost market value. On paper, SVB had enough assets to cover all deposits. But when the run began, selling those bonds at a loss created actual losses, which panicked more depositors, which forced more sales—a classic death spiral.

The Speed Factor: 1929 vs. 2023

Factor

1930s Bank Run

2023 SVB Run

Communication

Newspapers, word-of-mouth

Twitter, Slack, SMS

Time to coordinate

Days to weeks

Hours

Withdrawal method

Physical lines at branches

Mobile apps

Geographic spread

Local/regional

Instantly national

Speed of collapse

1-3 weeks

48 hours

The technology changed. The psychology did not.

“"The essential feature of a bank run is not that depositors believe the bank is insolvent, but that each depositor believes other depositors believe it.”

— Douglas Diamond, Nobel Laureate Economist

The FDIC: Psychology Masquerading as Insurance

After 9,000 American banks failed during the Great Depression, Congress created the Federal Deposit Insurance Corporation in 1933. The theory was elegant: if depositors know their money is insured, they will never have an incentive to run.

It worked. Bank runs virtually disappeared for nine decades. But the FDIC solved the psychology problem, not the structural one.

What FDIC Insurance Actually Covers

The FDIC insures deposits up to $250,000 per depositor, per bank, per ownership category. This covers:

Checking and savings accounts

Money market deposit accounts

Certificates of deposit (CDs)

Cashier's checks and money orders

It does NOT cover:

Stocks, bonds, or mutual funds

Cryptocurrency

Safe deposit box contents

Business accounts exceeding limits

Foreign currency deposits

[!NOTE] At Silicon Valley Bank, 96% of deposits exceeded the $250,000 FDIC limit. The average startup had $5-10 million in their account. The insurance that prevented bank runs for 90 years was irrelevant to the very depositors who triggered this one.

The Systemic Risk Exception

When SVB collapsed, the FDIC invoked a "systemic risk exception" to guarantee all deposits—insured or not. This was not mandated by law. It was a judgment call by regulators terrified that startup payrolls across America would freeze, triggering a broader crisis.

The bailout revealed an uncomfortable truth: FDIC insurance limits are a fiction for large institutions. When enough money is at stake, the government will override its own rules. But this guarantee is retrospective, not prospective. No depositor can know in advance whether their specific bank will receive special treatment.

The Digital Age: Bank Runs at the Speed of Light

The SVB collapse was not an anomaly. It was a preview.

Four Features That Make Modern Bank Runs Faster

Real-time balance visibility: In 1930, depositors could not know their bank's financial health. Today, bank financial statements are public, and analysts broadcast vulnerabilities on social media within hours.

Frictionless withdrawals: Moving money once required visiting a branch during business hours. Today, a founder can transfer $50 million from a beach in Bali at 2 AM.

Network effects: Venture capitalists share information in tight-knit group chats. When one influential investor tweets concern about a bank, their followers move immediately—before verifying the claim.

24-hour global markets: International depositors can initiate withdrawals while U.S. regulators sleep. By the time the FDIC opens Monday morning, a bank might already be drained.

[!INSIGHT] The average bank hold less than 10% of deposits in actual cash or cash equivalents. In a digital run, the money doesn't physically leave—it vanishes from the balance sheet in milliseconds, leaving regulators no time to organize a rescue.

The Crypto Example: Runs Without Regulators

Cryptocurrency platforms have demonstrated what bank runs look like without any FDIC backstop. When FTX collapsed in November 2022, users discovered they couldn't withdraw funds because the company had lent customer deposits to a trading firm owned by the CEO. No insurance. No recourse. Total loss.

This is what an unregulated banking system looks like. The FDIC does not prevent banks from failing. It prevents the failure from destroying depositors' lives. The crypto industry is learning this lesson the hard way, one exchange collapse at a time.

What This Means for Your Money

The modern banking system is safer than 1929—but not because banks are better managed. It is safer because regulators have more tools and willingness to intervene. But this safety is neither absolute nor predictable.

Practical Implications for Depositors

Diversify your banking: Keeping $2 million in one bank exposes you to uninsured risk. Spread deposits across multiple institutions.

Understand actual coverage: Business accounts, trust accounts, and joint accounts have different insurance calculations. The FDIC's "Electronic Deposit Insurance Estimator" tool can calculate your specific coverage.

Monitor bank health indicators: For large deposits, track your bank's capital ratios, loan-to-deposit ratio, and stock price. Early warning signs matter more than ever.

Accept that all banking involves risk: The 2023 crisis proved that even "safe" Treasury bonds can destroy a bank if sold at the wrong time. There is no such thing as a risk-free deposit.

Key Takeaway: Your bank is gambling with your money every day—betting that you won't ask for it back all at once. The FDIC insures most depositors up to $250,000, but the real protection is psychological: the belief that others won't run. In the age of Twitter and mobile banking, that belief can shatter in hours. The next bank run will be faster than the last.

*Sources: Federal Deposit Insurance Corporation, "History of the FDIC"; Silicon Valley Bank 2023 Failure Analysis, Federal Reserve; Diamond-Dybvig Model of Bank Runs, Journal of Political Economy (1983); Testimony of SVB CEO Greg Becker, U.S. Senate Banking Committee; Financial Stability Report, Federal Reserve Board (2023).

This is a Premium Article

Hylē Media members get unlimited access to all premium content. Sign up free — no credit card required.