On May 6, 2010, $1 trillion vanished in 36 minutes. No human pressed a button. This is how algorithms broke the market—and what it means for AI trading today.

Hyle Editorial·

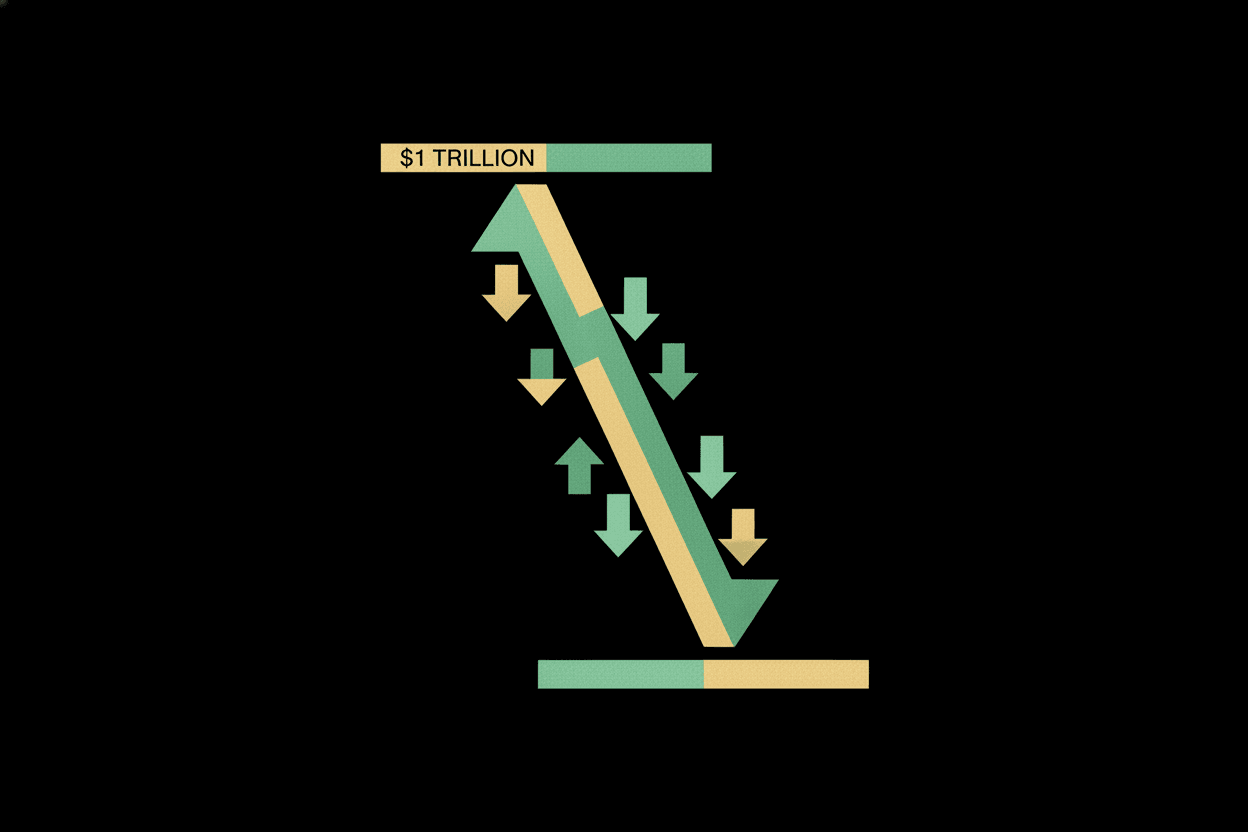

On May 6, 2010, $1 trillion in market value vanished in 36 minutes. No human made that decision. No human could stop it. At 2:32 PM, the Dow Jones sat comfortably at 10,486. By 2:47 PM, it had cratered to 9,869—a drop of nearly 1,000 points in under fifteen minutes. Procter & Gamble, a blue-chip stalwart, briefly traded for a penny. Accenture dropped from $42 to $0.01 in four seconds. Then, just as inexplicably, the market recovered. By 3:07 PM, most losses had been erased.

The official investigation took five months. The culprit wasn't terrorism, hacking, or human error in the traditional sense. It was a single algorithmic sell order from a mutual fund company that triggered a catastrophic feedback loop among high-frequency trading systems. The machines, programmed to react faster than any human could think, had panicked together—and revealed a terrifying vulnerability at the heart of modern finance.

At 2:32 PM Eastern time, a Kansas-based mutual fund company initiated an algorithm to sell 75,000 E-mini S&P 500 futures contracts—a position worth approximately $4.1 billion. The algorithm was designed to execute the sale over the entire trading day, but its sell-pressure sensor had a fatal flaw: it accelerated selling when prices dropped, creating a self-reinforcing downward spiral.

What happened next stunned regulators and traders alike. High-frequency trading (HFT) algorithms, which account for over 60% of U.S. equity volume, detected the massive sell pressure and began front-running the order. They sold to each other in rapid succession, creating what the Commodity Futures Trading Commission (CFTC) later called a "hot potato" effect—in less than 14 seconds, over 27,000 contracts changed hands among HFT firms.

[!INSIGHT] In the 14 seconds between 2:45:13 and 2:45:27, high-frequency traders exchanged contracts at an average rate of 2,000 per second—all while genuine buyers had completely vanished from the market.

The liquidity that HFT firms claimed to provide evaporated precisely when it was needed most. Market makers, sensing extreme volatility, widened their spreads or withdrew entirely. With no human oversight capable of intervening in sub-second timeframes, the feedback loop accelerated.

The Liquidity Vacuum

The flash crash revealed a structural flaw in algorithm-driven markets. When all participants use similar strategies—momentum following, statistical arbitrage, volatility targeting—they become correlated in crisis. The very speed that makes HFT profitable becomes toxic in a cascade.

“*"The market structure we built assumed that more speed and more algorithms meant more efficiency. On May 6, we learned that it can also mean collective insanity.”

— Andrew Lo, MIT Financial Economist

Consider this: during the worst of the crash, some stocks traded at prices that defied any rational valuation. Exelon Corporation dropped 99.9% in minutes. Sotheby's spiked to $99,999.99 per share—its previous close was $34. These weren't isolated glitches but symptoms of a market where algorithms had become the only participants, talking only to each other.

The Regulatory Aftermath

The CFTC and SEC joint report, released in October 2010, laid blame on a confluence of factors: the oversized sell order, HFT feedback loops, and the absence of circuit breakers at the individual stock level. The findings led to significant changes:

Limit Up-Limit Down Rules: Implemented in 2012, these prevent trades outside specified price bands.

Market-Wide Circuit Breakers: Now trigger 15-minute pauses at 7%, 13%, and 20% declines in the S&P 500.

Enhanced Audit Trails: The Consolidated Audit Trail (CAT) now tracks all orders and trades with timestamp precision.

Yet critics argue these are band-aids on a deeper wound. Speed still dominates. Algorithms still interact without human mediation. And the fundamental problem—correlated automated responses to stress events—remains unsolved.

[!NOTE] Similar flash crashes have occurred since: the August 24, 2015 equity selloff, the October 15, 2014 Treasury bond flash rally, and the January 2019 Japanese yen "flash crash." Each time, algorithms were implicated.

What Flash Crash Teaches Us About AI and Markets

The 2010 flash crash was not merely a technical malfunction—it was a preview of systemic risks that have only grown as artificial intelligence penetrates financial markets. Today's AI trading systems are vastly more sophisticated than the 2010 algorithms. They use deep learning, reinforcement learning, and alternative data sources. But the core vulnerability remains.

The Illusion of Control

Modern AI systems can process market signals in microseconds, execute complex multi-asset strategies, and adapt to changing conditions in real-time. Yet they lack what humans possess: situational awareness beyond historical patterns, the ability to question assumptions, and the capacity to refuse to trade when conditions make no sense.

When multiple AI systems operate in the same market, trained on similar data, optimizing for similar objectives, they become an emergent system with unpredictable properties. The 2010 flash crash was this emergence in its simplest form—algorithms reacting to algorithms. Today's AI ecosystems are exponentially more complex, and exponentially more opaque.

“*"We have moved from a world where humans trade with humans, to algorithms trading with algorithms, to AI systems learning from AI systems. At each step, the chain of accountability grows longer and more fragile.”

— SEC Commissioner testimony, 2023

The Black Box Problem

The 2010 investigation took five months to reconstruct what happened in 36 minutes. Today's AI trading systems use models that even their creators cannot fully explain. When an AI fund loses billions—or wins billions—there is often no human who can articulate the precise reasoning chain. This opacity poses existential questions for market integrity.

Implications: Living with Machine Markets

The flash crash of 2010 settled a debate that had been raging since electronic trading began. Algorithms are not neutral tools—they are market participants with their own behavioral patterns, their own biases, their own capacity for collective irrationality. The question is no longer whether machines can replace human judgment in trading. They already have. The question is whether we can build systems robust enough to contain machine panic.

For investors, the lesson is sobering. In a crisis, you may not be able to sell at any price—not because no one wants your asset, but because the machines have all decided simultaneously to stop buying. For regulators, the challenge is to oversee systems that evolve faster than rules can be written. For technologists, the flash crash remains a warning: optimization without understanding systemic effects is not intelligence—it's fragility dressed as efficiency.

Key Takeaway

The 2010 flash crash proved that algorithmic markets can exhibit emergent crises no human can anticipate or prevent. As AI systems grow more autonomous and interconnected, the risk shifts from individual failures to systemic events where machines panic together—faster than any human can respond. The next crash won't be about one bad algorithm. It will be about an ecosystem of AI traders all learning the same wrong lesson at the same time.

Sources: CFTC-SEC Findings Regarding the Events of May 6, 2010; Kirilenko, Kyle, Samadi, Tuzun (2017) "The Flash Crash: The Impact of High Frequency Trading on an Electronic Market"; Aldridge (2013) High-Frequency Trading: A Practical Guide to Algorithmic Strategies and Trading Systems; SEC Commissioner Allison Lee testimony on AI and Market Structure, 2023

This is a Premium Article

Hylē Media members get unlimited access to all premium content. Sign up free — no credit card required.