92% of the World's Advanced Chips Come From One Island

92% of advanced chips are made in Taiwan by TSMC. This geographic concentration wasn't planned—it's modern civilization's single greatest vulnerability.

The Most Dangerous Monopoly in Human History

Every advanced AI chip, every iPhone processor, every server powering the internet—92% of them are made in one country, by one company, on one island that China officially considers its own territory. This is not a supply chain risk. This is a single point of failure for modern civilization.

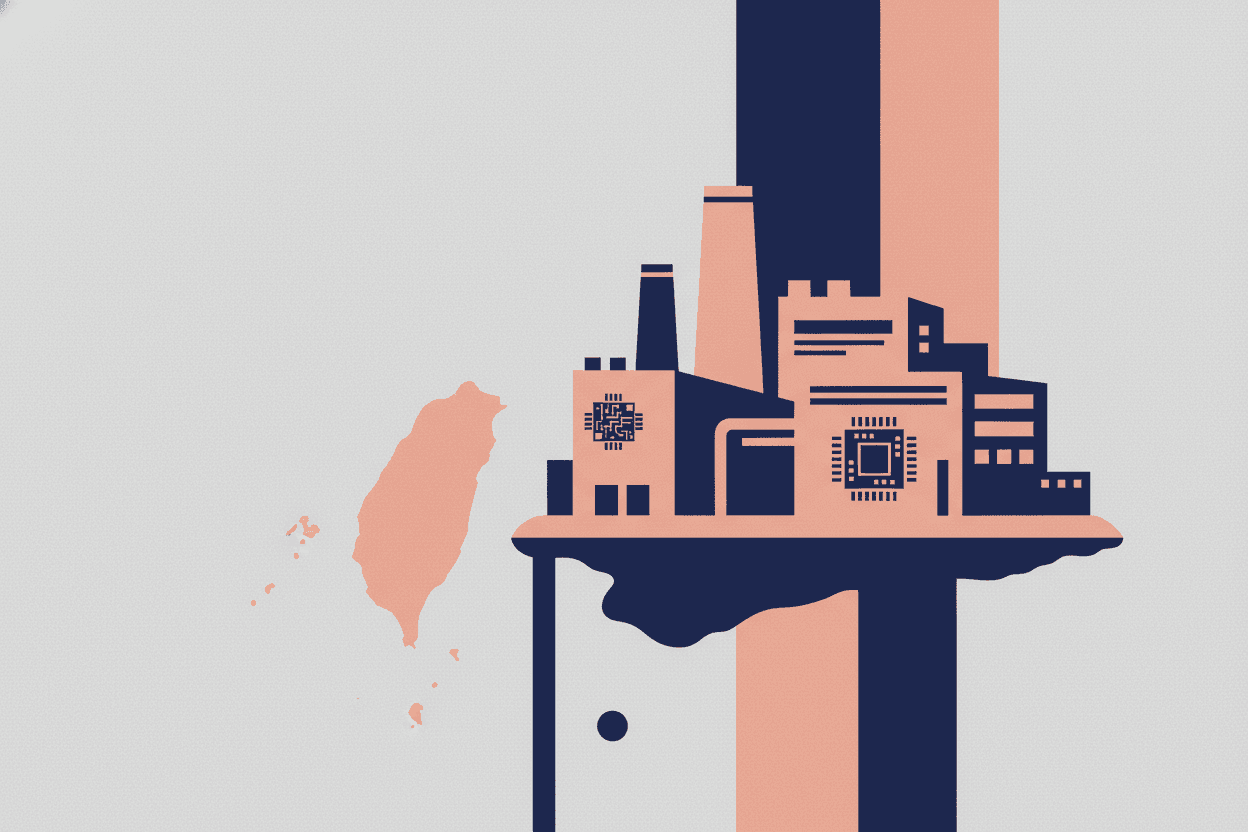

In 2024, Taiwan Semiconductor Manufacturing Company (TSMC) produced 92% of the world's semiconductors manufactured at process nodes below 10 nanometers. Not a majority. Not a dominant share. Ninety-two percent. The remaining 8% comes primarily from Samsung in South Korea and Intel in the United States, with Intel struggling to ramp its most advanced production.

The question keeping Pentagon strategists and Silicon Valley CEOs awake at night is not whether this concentration poses a risk. The question is why the world allowed this to happen—and whether anything can be done about it before geopolitical reality catches up with industrial vulnerability.

How Taiwan Won the Semiconductor Lottery

The year was 1987. Morris Chang, a Texas Instruments veteran, founded TSMC with a revolutionary business model: pure-play foundry manufacturing. Unlike Intel or Samsung, which designed and manufactured their own chips, TSMC would manufacture chips designed by others.

[!INSIGHT] The foundry model democratized chip design. Companies without billions in manufacturing capital—NVIDIA, Qualcomm, Apple—could still compete at the cutting edge. TSMC became the arms dealer of the digital age.

This model created a flywheel effect. More customers meant more revenue for R&D. Better technology attracted more customers. By 2014, when TSMC began mass production of 16nm FinFET technology, the company had established an insurmountable lead in manufacturing yield and cost efficiency.

But technology alone doesn't explain Taiwan's dominance. The island possessed three critical advantages:

-

Talent Density: Taiwan produces more engineers per capita than almost any nation. The electrical engineering program at National Taiwan University receives 30,000 applications annually for 200 positions.

-

Ecosystem Clustering: Within a 50-kilometer radius of Hsinchu Science Park, you find ASML's lithography machines, Applied Materials' deposition equipment, and thousands of specialized suppliers. Nowhere else on Earth can you prototype a chip, source materials, and scale to mass production faster.

-

Government Support: Taiwan's government provided $5.5 billion in subsidies for TSMC's 3nm fab expansion. The company pays an effective corporate tax rate roughly half of what it would in the United States.

“"We didn't plan to dominate. We planned to survive. Dominance was the byproduct of doing one thing better than anyone else for thirty-five years.”

By 2020, when Apple needed 5nm chips for the M1 processor, only TSMC could deliver at scale. When NVIDIA needed 4nm chips for H100 AI accelerators that would power the generative AI revolution, only TSMC had the capacity. The world's most valuable companies became utterly dependent on a single supplier.

The Geography of Catastrophic Risk

Taiwan sits 160 kilometers from mainland China. The Taiwan Strait, 180 kilometers wide at its narrowest point, separates two governments claiming sovereignty over the same territory. The People's Republic of China has never renounced the use of force to achieve reunification.

A blockade of Taiwan—military or economic—would not merely disrupt chip supplies. It would halt production of virtually every advanced electronic device within months. Consider the cascading effects:

-

Smartphones: Apple sells 200 million iPhones annually. Each contains an A-series processor manufactured exclusively by TSMC. Inventory buffers typically last 4-6 weeks.

-

Data Centers: Amazon, Microsoft, Google, and Meta collectively spend over $150 billion annually on data center infrastructure. Without TSMC-manufactured GPUs and CPUs, cloud computing expansion stops.

-

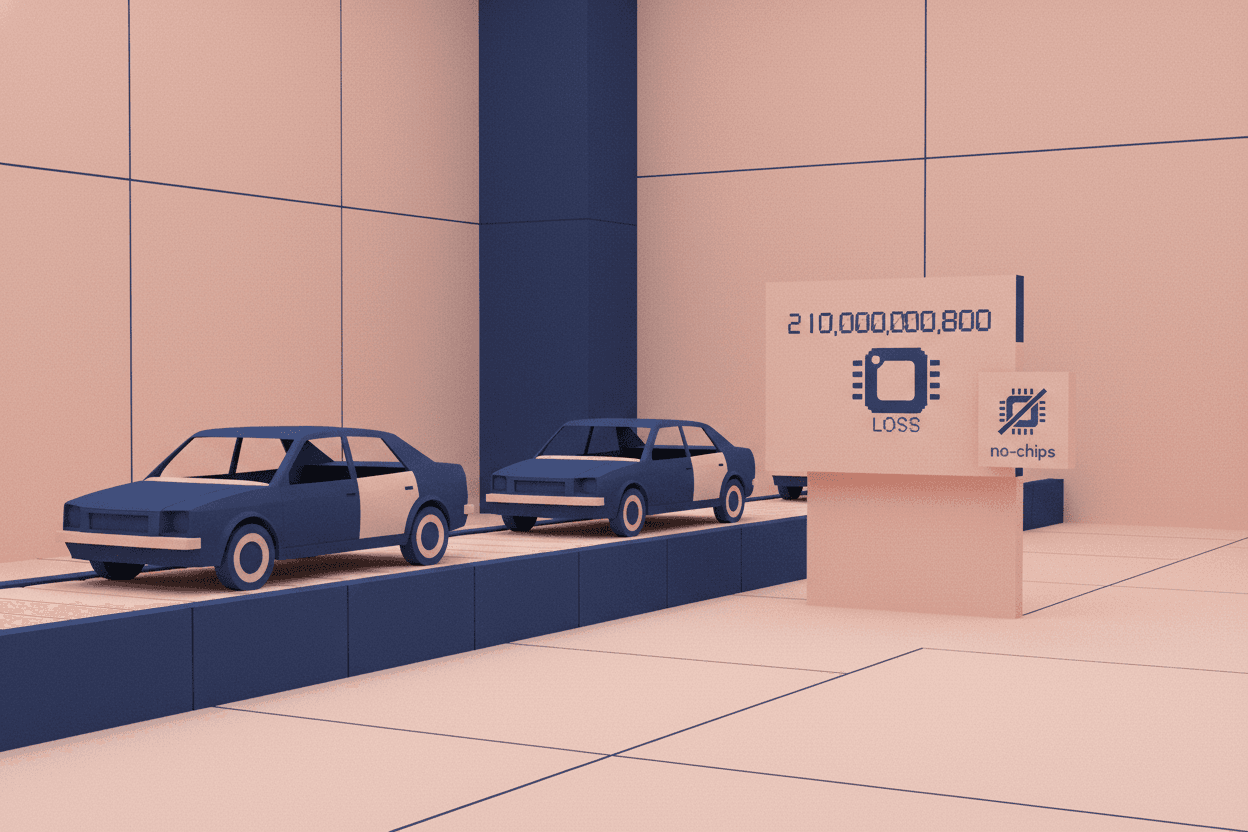

Automotive: Modern vehicles contain 1,000-3,000 chips. In 2021, a far less severe chip shortage caused global automakers to cut production by 11.3 million vehicles and lose $210 billion in revenue.

[!INSIGHT] The 2021 semiconductor shortage was caused by a 10% supply-demand gap. A Taiwan disruption would create a 40-60% gap for advanced chips. There is no historical precedent for such a shock.

The RAND Corporation modeled a six-month Taiwan chip shutdown. Their estimate: $2.5 trillion in global economic damage in the first year alone. For comparison, the 2008 financial crisis erased $2 trillion in global GDP.

Why Nobody Stopped This

The concentration of advanced chip manufacturing in Taiwan wasn't a conspiracy. It was a market failure compounded by strategic blindness.

American semiconductor companies, following shareholder primacy doctrine, outsourced manufacturing to reduce capital expenditure. Why spend $20 billion on a fab when TSMC would build it for you? Between 1990 and 2020, America's share of global semiconductor manufacturing fell from 37% to 12%.

[!NOTE] The CHIPS and Science Act of 2022 allocated $52 billion to rebuild American semiconductor manufacturing. TSMC's Arizona fab, originally planned for 2024 production, has been delayed to 2025 or later due to labor shortages and cost overruns. Building fabs is easier than building the expertise to run them.

European governments made similar miscalculations. ASML, the Dutch company that manufactures the extreme ultraviolet lithography machines essential for advanced chips, operates as a virtual monopoly. But ASML machines are useless without the engineers who operate them—and the institutional knowledge of how to integrate them into high-yield production lines.

Samsung remains the only credible competitor to TSMC at the most advanced nodes. But Samsung's foundry business has struggled with yield issues at 3nm. In 2023, industry reports suggested Samsung's 3nm yields were below 20%, compared to TSMC's reported 60-70%.

Intel, once the world's most advanced chip manufacturer, spent a decade focused on optimizing legacy products while TSMC and Samsung advanced. Under CEO Pat Gelsinger, Intel has committed to becoming a foundry provider by 2025—but the company's 18A process node remains unproven at scale.

The Uncomfortable Reality

TSMC is expanding. New fabs in Arizona, Japan, and Germany are under construction. By 2027, the company projects that 20-25% of its advanced manufacturing capacity will be outside Taiwan.

But capacity and capability are not the same. The Arizona fab will produce 4nm chips—technology TSMC has already mastered. The most advanced 2nm and A16 nodes will remain in Taiwan for the foreseeable future. The knowledge ecosystem, the supplier networks, and the specialized workforce cannot be replicated in five years.

The geopolitical clock is ticking. U.S. military planners reportedly estimate a peak window for Chinese action against Taiwan between 2025 and 2027. Whether this intelligence is accurate or not, the perception alone shapes corporate and governmental behavior.

“[!INSIGHT] TSMC has become what analysts call a "silicon shield”

The world's most valuable company, Apple, is wholly dependent on TSMC. The world's most important AI company, NVIDIA, is wholly dependent on TSMC. The world's most powerful military, the United States Department of Defense, sources critical chips from TSMC through intermediaries. This is not market efficiency. This is systemic fragility.

What Comes Next

Three scenarios will determine whether the semiconductor concentration becomes a crisis or a catalyst for change.

Scenario 1: Successful Diversification. The CHIPS Act, combined with TSMC's expansion and Intel's foundry ambitions, creates meaningful competition by 2030. No single location controls more than 50% of advanced manufacturing. Risk is reduced but not eliminated.

Scenario 2: Status Quo Decay. Geopolitical tensions persist without open conflict. TSMC maintains dominance while alternatives struggle to achieve scale. The world lives with elevated risk, hoping for the best.

Scenario 3: Disruption Event. Blockade, natural disaster, or conflict interrupts Taiwan production. The global economy experiences a shock exceeding 2008. Governments implement emergency measures—chip rationing, priority allocation for defense and critical infrastructure.

Sources: Semiconductor Industry Association, Boston Consulting Group "Turn the Tide" Report (2024), RAND Corporation Taiwan Contingency Analysis, Bloomberg Supply Chain Data, Taiwan Ministry of Economic Affairs Statistics, Company Filings (TSMC, Samsung, Intel)