The 2021 chip shortage cost automakers $210 billion. That was a 6% supply dip. What happens when Taiwan's fabs go dark? The cascade is incomprehensible.

Hyle Editorial·

During the 2021 chip shortage — caused by a temporary demand spike, not a geopolitical crisis — Ford lost $2.5 billion, GM shut factories, and people paid $1,200 for a $500 PlayStation. That was a 6% supply reduction. Model what a 92% reduction looks like. The word 'shortage' doesn't cover it.

In the first quarter of 2021 alone, the global automotive industry idled production lines capable of producing 1.4 million vehicles. Not because steel was scarce. Not because labor went on strike. Because a component the size of a fingernail couldn't be sourced. Samsung Electronics, caught in the same squeeze, warned that the crisis could disrupt smartphone production through 2022. Hospitals reported delays in ventilator deliveries. The U.S. Defense Department flagged concerns about replenishing precision-guided munitions. And this was a ripple. What happens when the source of 92% of the world's most advanced semiconductors goes offline?

The semiconductor shortage of 2021-2022 was not predicted. It emerged from a perfect storm: pandemic-driven demand for home electronics collided with just-in-time inventory systems that had zero resilience built in. Automakers, having canceled chip orders early in the pandemic expecting a vehicle sales collapse, found themselves at the back of the queue when demand roared back.

The numbers are staggering. Ford reported a $2.5 billion hit to operating income in 2021. General Motors paused production at eight assembly plants across North America. Volkswagen scaled back output in China. Toyota, the world's most efficient manufacturer, slashed production by 40% in September 2021. Total lost auto revenue globally exceeded $210 billion.

[!INSIGHT] The 2021 crisis involved mature node chips — the legacy semiconductors used in cars, appliances, and industrial equipment. Advanced logic chips, the kind manufactured almost exclusively in Taiwan, were less affected. A Taiwan disruption hits both categories simultaneously.

The consumer electronics sector fared no better. Sony launched the PlayStation 5 in November 2020 with an initial production run of roughly 5 million units. Demand exceeded 50 million. Scalpers resold consoles at 200% premiums. GPU prices tripled. A secondary market emerged where graphics cards became speculative assets.

The Hospital Problem No One Discusses

Medical devices were caught in the crossfire. Ventilators, patient monitors, MRI machines — all depend on semiconductors that were suddenly unavailable. In 2021, Philips reported delays in delivering hospital equipment. GE Healthcare warned of imaging system shortages. None of this made headlines the way car plant closures did, but the implications are more dire: when you cannot source chips for medical devices, people do not just pay more. They wait longer for diagnoses. Some of them die.

The defense sector also felt the pressure. The U.S. military sources thousands of components that require semiconductors, from communication systems to missile guidance. In testimony before Congress, defense officials acknowledged that replenishment cycles for certain munitions had extended dangerously. This from a supply shock that no adversary engineered.

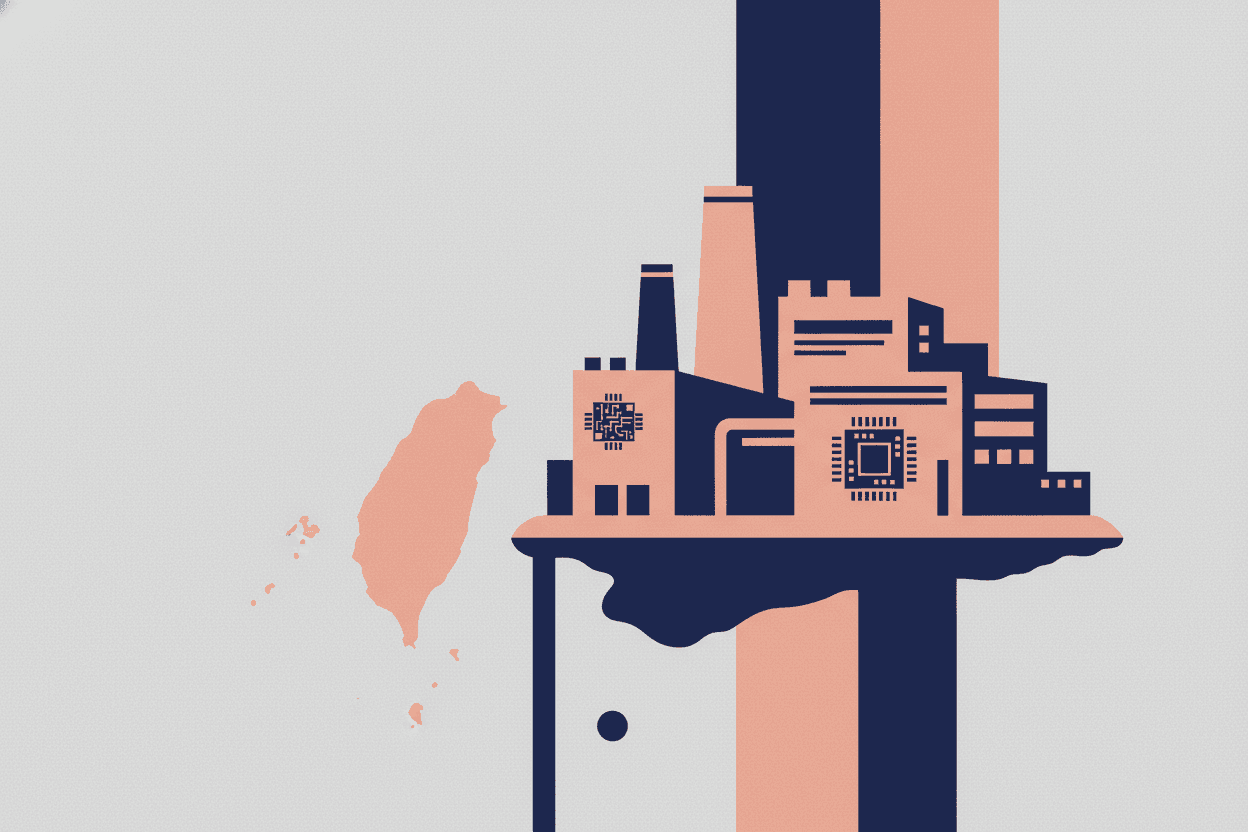

The Taiwan Concentration Problem

Taiwan Semiconductor Manufacturing Company (TSMC) alone fabricates approximately 92% of the world's most advanced logic chips — semiconductors below 10 nanometers that power everything from smartphones to AI training clusters. The island accounts for roughly 65% of all foundry revenue globally and nearly 90% of advanced packaging capacity.

“*"If Taiwan were unable to manufacture chips for a year, the global electronics industry would essentially shut down. The economic damage would be measured in trillions, not billions.”

— Chris Miller, author of 'Chip War'

This concentration is historically anomalous. No other critical industry has this level of geographic single-point failure. Saudi oil production at its peak accounted for perhaps 25% of global supply. Taiwan's share of advanced chips is nearly four times that.

The Dependency Map

Consider what passes through Taiwan's fabrication facilities:

Consumer Electronics: Apple's A-series and M-series chips, Qualcomm's Snapdragon processors, AMD's Ryzen and EPYC CPUs, Nvidia's data center GPUs — all manufactured primarily by TSMC. A six-month halt means no new iPhones, no new laptops, no new gaming consoles. Existing inventory would deplete in weeks.

Automotive: Modern vehicles contain 1,000 to 3,000 chips each. Electric vehicles require even more. The advanced driver assistance systems, battery management, infotainment — all depend on semiconductors that trace back to Taiwan either directly or through supply chain dependencies.

Data Centers: Amazon Web Services, Microsoft Azure, Google Cloud, Oracle Cloud — the infrastructure that runs the internet — depends on a continuous supply of server CPUs and accelerators. Cloud capacity growth would halt. Existing workloads would face increasingly constrained resources.

Defense Systems: The F-35 fighter jet contains thousands of chips. Precision-guided munitions, satellite communication, radar systems, encryption hardware — the modern military runs on semiconductors. A prolonged disruption cannot be substituted through stockpiles.

Medical Devices: MRI machines, CT scanners, robotic surgical systems, pacemakers, insulin pumps, diagnostic equipment. The healthcare system has been digitizing for decades. That digital infrastructure has a physical dependency most administrators never consider.

The Cascade Effect

A six-month cessation of Taiwan's semiconductor output would not simply cause shortages. It would trigger cascading failures across interconnected systems. The dominoes do not fall in sequence. They fall simultaneously.

[!NOTE] Just-in-time manufacturing, which revolutionized industrial efficiency, has eliminated the buffer that once existed. Average semiconductor inventory for electronics manufacturers fell from 40 days in 2010 to less than 10 days by 2020. There is no slack in the system.

Month One: Existing chip inventory depletes. Consumer electronics manufacturers halt new product lines. Automakers begin plant closures within weeks, not months. Spot prices for available semiconductors increase 500-1,000%.

Month Two: Cloud providers stop accepting new customers. Existing workloads face performance degradation. Companies that canceled on-premise servers in favor of cloud flexibility discover the downside of dependency.

Month Three: Medical device manufacturers cannot fulfill orders. Hospitals delay equipment replacement. Elective procedures dependent on advanced imaging face indefinite postponement.

Month Four: Defense contractors notify governments of replenishment delays. Military readiness assessments get classified. Stock prices for every technology company collapse simultaneously.

Month Five: Secondary effects dominate. Restaurants using digital payment systems face terminal failures with no replacements. Logistics companies cannot source tracking hardware. The Internet of Things stops growing.

Month Six: Economic contraction exceeds 2008 levels. Unemployment in technology-adjacent industries spikes. Governments face pressure no policy toolkit addresses.

Why Resilience Failed

Following the 2021 shortage, governments and corporations pledged to diversify semiconductor sourcing. The CHIPS Act in the United States authorized $52 billion to encourage domestic fabrication. The European Union announced a €43 billion Chips Act. TSMC committed to building facilities in Arizona and Japan. Samsung expanded in Texas.

None of this solves the problem.

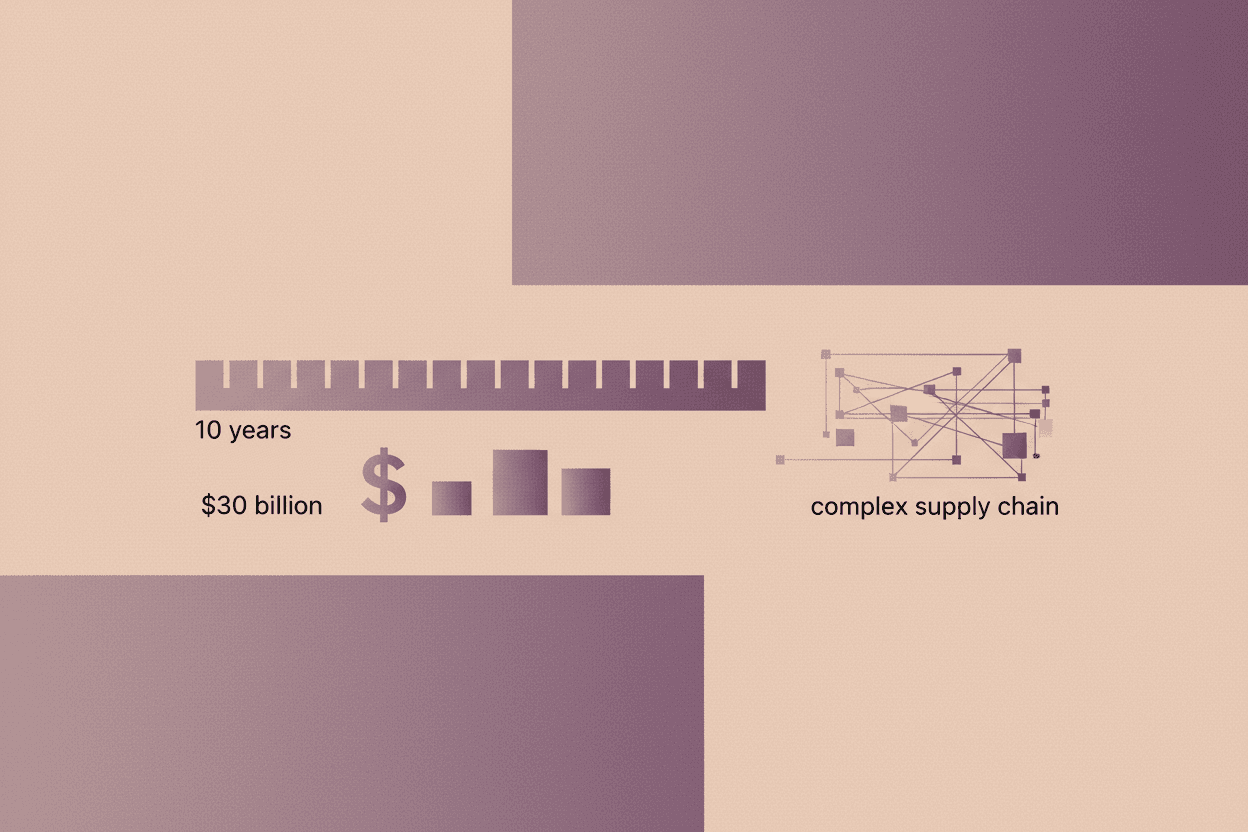

New fabrication facilities take 3-5 years to become operational. The Arizona TSMC plant, announced in 2020, began construction in 2021 and will not reach volume production until 2025 at earliest. Even then, initial capacity represents a fraction of Taiwan output. The skilled workforce required — technicians, engineers, process specialists — does not exist in sufficient numbers outside Taiwan and must be trained over years.

[!INSIGHT] Advanced semiconductor fabrication requires not just capital but tacit knowledge accumulated over decades. The yield rates — the percentage of chips that function correctly — depend on institutional expertise that cannot be replicated by funding alone. A fab built is not a fab capable.

The industry response to 2021 was rational at the company level and inadequate at the system level. Automakers secured long-term supply agreements. Electronics manufacturers diversified suppliers. But diversifying among suppliers that all depend on Taiwan fabrication creates an illusion of resilience. The map of dependencies was redrawn. The concentration risk remained.

The Uncomfortable Recognition

The 2021 chip shortage was a warning that most interpreted incorrectly. It was not a temporary disruption revealing the need for better inventory management. It was a preview of structural fragility that no inventory policy addresses.

Civilization has bet its critical infrastructure on a supply chain with a single point of failure. Energy, transportation, healthcare, communication, finance, defense — all depend on semiconductors. Those semiconductors depend on Taiwan. The probability of a major disruption may be debated. The consequence of one cannot be.

Key Takeaway: The 2021 chip shortage was not a crisis. It was a mild constraint that cost the global economy $210 billion. A genuine crisis — Taiwan fabrication offline for six months — would not cause shortages. It would cause failures. The word for that is not 'inconvenience.' The word is 'collapse.' The time to build resilience was ten years ago. The second-best time is now. But building takes years we may not have.

Sources: S&P Global Automotive Report 2021; Sony Financial Statements Q3 2021; Boston Consulting Group 'Semiconductor Supply Chain' Analysis; Chris Miller, 'Chip War: The Fight for the World's Most Critical Technology' (2022); U.S. Department of Defense Industrial Base Report; Taiwan Ministry of Economic Affairs Data; Philips Q2 2021 Earnings Call; Congressional Testimony on Defense Industrial Base, 2021

This is a Premium Article

Hylē Media members get unlimited access to all premium content. Sign up free — no credit card required.