Why Keeping Cash Under the Mattress Is Sometimes Rational

In 2013, the EU legally confiscated bank deposits to save failing banks. Discover how modern 'bail-in' laws work and why your savings are unsecured loans.

In 2013, the European Union froze Cypriot bank accounts and converted a massive percentage of large deposits into bank shares without asking for permission. This was entirely legal. Today, it is official EU policy. The term for this maneuver is a 'bail-in.' And the term for your bank deposit is, legally speaking, an unsecured loan to a highly leveraged financial institution.

During the peak of the Cyprus banking crisis, depositors at the Bank of Cyprus experienced a shock that shattered modern financial assumptions: a staggering 47.5% of their uninsured funds above €100,000 were forcibly seized to recapitalize the failing institution. Overnight, ordinary citizens, local businesses, and retirees saw their liquid cash transformed into highly illiquid equity in a collapsing bank. In exchange for their life savings, they became reluctant shareholders.

Since that fateful weekend, global financial regulators have quietly shifted the rulebook. From the EU's Bank Recovery and Resolution Directive (BRRD) to provisions within the US Dodd-Frank Act, the bail-in has become a standard regulatory tool. We are constantly reassured that deposit insurance makes our money perfectly safe. But what exactly does that insurance guarantee when the banking sector threatens to take down the sovereign state itself? If the ultimate backstop fails, are you a conservative saver, or an unwitting venture capitalist funding your bank's risky bets?

The Legal Reality of a Bank Deposit

Most people operate under a fundamental misunderstanding of what a bank account actually is. When you hand physical cash to a teller or receive a direct deposit from your employer, you are not placing money into a vault with your name on it. You are entering into a creditor-debtor relationship.

[!INSIGHT] The moment your money enters a bank account, it ceases to be your property. Legally, you have executed an unsecured loan to the bank. The balance you see on your screen is merely an IOU—a liability on the bank's balance sheet, promising to pay you back upon request.

Because your loan to the bank is 'unsecured,' it is not backed by specific collateral. If the bank mismanages its assets—by issuing bad loans, buying underwater sovereign bonds, or making catastrophic bets on interest rates—and enters insolvency, you must stand in line with other creditors in bankruptcy court.

Historically, governments panicked at the thought of depositors losing their money, leading to the era of 'bail-outs.' But after the 2008 Great Financial Crisis, taxpayer tolerance for rescuing billionaire bankers plummeted. Politicians needed a new solution. They found it in Cyprus.

The Shift: From Bail-Out to Bail-In

A bail-out uses external taxpayer money to rescue a failing bank. A bail-in, by contrast, forces the bank's own creditors and depositors to absorb the losses.

When a bank's liabilities exceed its assets, regulators can step in and arbitrarily write down the value of unsecured debt—including customer deposits—or convert that debt into equity to balance the books.

“"If there is a risk in a bank, our first question should be 'Okay, what are you in the bank going to do about that? What can you do to recapitalise yourself?' If the bank can't do it, then we'll talk to the shareholders and the bondholders, we'll ask them to contribute in recapitalising the bank, and if necessary the uninsured deposit holders.”

Following the Cyprus template, the Financial Stability Board (FSB) mandated that Global Systemically Important Banks (GSIBs) must issue specific debt instruments designed to be bailed in. But if those buffers are exhausted, the law allows regulators to target corporate payroll accounts and individual savings.

The Anatomy of a Bail-In

When a bank faces imminent collapse under the modern resolution framework, regulators typically follow a brutal mathematical sequence:

- Step 1: Wipe Out Shareholders: Existing equity is zeroed out. The original owners lose everything.

- Step 2: Burn the Bondholders: Subordinated debt and hybrid capital instruments are written off or converted to equity.

- Step 3: Target the Depositors: If the capital hole is still not filled, large, uninsured deposits are seized and converted into shares of the newly restructured (and highly stigmatized) bank.

The Limits of Deposit Insurance

Defenders of the modern banking system point to deposit insurance—such as the FDIC in the United States (covering up to $250,000) or the European Deposit Insurance Scheme (covering up to €100,000)—as the ultimate shield. As long as you stay under the limit, your money is safe from a bail-in. Or so the theory goes.

[!NOTE] Deposit insurance funds are surprisingly shallow. The FDIC's Deposit Insurance Fund (DIF) typically maintains a reserve ratio of just 1.15% to 1.35% of total insured deposits. They do not have the capital to cover a systemic banking collapse; they only have enough to handle isolated, idiosyncratic bank failures.

When a true systemic crisis hits, the deposit insurance fund empties rapidly. At that point, the insurance agency must borrow from the Treasury—meaning the sovereign government steps in. But what happens if the sovereign itself is financially distressed?

In Cyprus, the government could not afford to bail out its oversized banking sector without bankrupting the state. The sovereign was insolvent, which meant the deposit guarantee was effectively worthless for the banking system as a whole. The EU forced the bail-in precisely because no one else could foot the bill.

Implications: Sovereign Risk and the Mattress

The Cyprus event proved that deposit insurance is only as strong as the fiscal health of the government backing it. In an era of record-high sovereign debt, chronic deficit spending, and creeping inflation, the assumption that a government can infinitely print money to backstop bank deposits is being tested.

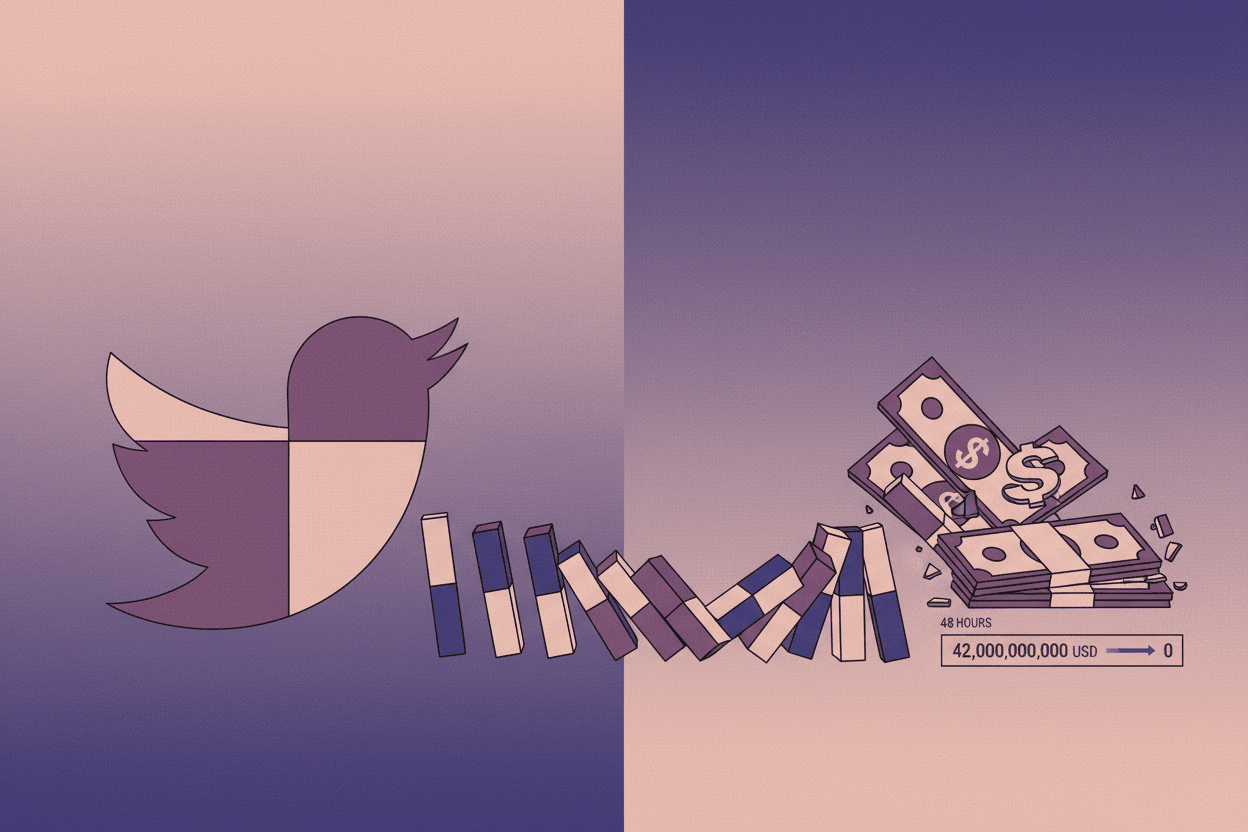

If the state's creditworthiness comes into question, capital flight accelerates. And because modern banking is entirely digital, a bank run that used to take weeks of people standing in physical lines can now happen in hours via smartphone apps—as seen in the rapid collapse of Silicon Valley Bank in 2023.

For high-net-worth individuals, corporate treasurers, and cautious savers, this legal reality changes the calculus of risk. Suddenly, holding zero-yielding physical assets—gold, real estate, or even cash 'under the mattress'—is not merely an act of paranoia. It is a rational diversification strategy against counterparty risk. Physical cash and bearer assets do not have a counterparty. They cannot be legally reclassified as bank equity by a desperate regulator on a Sunday night.

Sources: European Commission Bank Recovery and Resolution Directive (BRRD); Financial Stability Board (FSB) Key Attributes of Effective Resolution Regimes; Statements from the Eurogroup on Cyprus (2013); FDIC Quarterly Banking Profile.